Research Article - (2022) Volume 11, Issue 2

Received: 18-Feb-2022, Manuscript No. IJEMS-22-54930;

Editor assigned: 20-Feb-2022, Pre QC No. P-54930;

Reviewed: 05-Mar-2022, QC No. Q-54930;

Revised: 07-Mar-2022, Manuscript No. R-54930;

Published:

14-Mar-2022

, DOI: 10.37421/2162-6359.2022.11.625

Citation: Atsu, Victor Marvelous. Corporate Governance a Predictor of Banks Failure: Evidence from Registered Commercial Banks in Ghana. Int J Econ Manag Sci 11 (2022): 625.

Copyright: © 2022 Atsu VM. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

The quantitative study sought to identify corporate governance elements that precipitate commercial banks failure in Ghana and to outline policy recommendations to address those factors to make commercial banks more resilient and profitable. The quantitative study seeks to contribute to the body of knowledge by providing understanding on factors that contributes to banks failure in emerging economy like Ghana. A random sampling approach was used to collect annual report and published financial statement on 21 commercial banks. Based on this data, a fiveyear (5) panel data was formed: using a data range (2012 -2016 multiplied by 21 sampled banks) making a total of one hundred and five (105) observations. A random effect model was used to estimate the relationship between corporate governance elements and banks failure. Next, a correlation analysis was employed to examine the relationships between corporate governance elements, banks-specific financial proxies and exogenous factors and banks failure. Results from the study indicate a significant relationship between corporate governance variables, banks-specific financial information and macroeconomic indicators and banks failure. The study recommends the creation of Ghanaian corporate governance act to propose and increase in the female representation on the governing boards of commercial banks. This measure is to increase gender diversity and skills in the boardroom as it is evident in the study that higher gender diversity reduces the risk of banks failure. More so, the study recommends an effective management of credit default rate (using credit default swap to mitigate credit losses and) to boost financial soundness and profitability of banks in Ghana.

Corporate governance act • Governing board size • Female executive directors • Credit default swap • Banks financial proxies • Macro economic indicators

In the past the national economy of Ghana was faced with grave economic downturn, this occurs between 1970 - 1983. This economic development was largely ascribed to acute shortage of oil supplies in the 1970 and the infamous bushfires that occurred in the early part of 1983. This situation was further intensified by the return of Ghanaian migrants from Nigeria in the late part of 1980 [1,2]. A combination of these factors together with weak government fiscal position and harsh external factors (such as, high exchange rate and high prices for imported commodities) created grave discrepancies in the fiscal space of government at the time [2]. Regrettably, the tendency of economic misfortunes at the time extended its grave waves to the Ghanaian banking industry such that there was lack of confidence in the banking products and generally this saves as a disincentive to domestic savings [2]. This unfortunate economic situation was not limited to the Ghanaian economy but also extended its mass destructive waves to other world economies and has caused the sudden demise of Enron Corporation and Lehman Brothers [3].

Samanhyia, et al. [3] cited eight (8) commercial banks that got collapsed in Ghana between 2000-2008 representing an average failure rate of 12.5% (1/8 banks x 100) = 12.5%. Gatsi and Giordani, et al. [4,5] indicated such circumstances under which banks could become insolvent when banks failed to meet short term commitment to customers such that return on equity (RoE), return on assets (RoA), share of industry assets (SoIA) are respectively low. Under such a situation credit default rate (CDR) is high; capital adequacy ratio (CAR) is low and liquidity ratio low. These factors may compound further the level of deterioration in the exogenous factors such that inflation (IFL) and taxation (TAX) are high and gross domestic product (GDP) slumps [6]. The multiplying effect is that banks can not cover every one USD ($1) invested by equity holders and becomes distressed without assets [7]. Appiah, et al. [8] and Taffler [9] stressed that banks insolvency investigation is on the ascendancy and features significantly in the governance debate around the globe. Betts and Belhoul [10] noted that the corporate governance procedures of banks are important checks and balances that serves as a guideline for administering the affairs of a bank with the view to maximize stockholder wealth. Appiah [11] considered corporate governance as a well delineated arrangement, methods, practices, philosophies and value systems aimed at mitigating agency problem to maximize shareholder wealth.

Mahama [12] and Samanhyia, et al. [3] indicated that the global phenomenon of financial devastation had its highest toll on Ghana's national economy as listed commercial banks were exposed to external shocks in the past decade and this has caused mass banks failure. Between 2000- 2008, there were eight (8) major commercial bank failure in Ghana and ten (10) microfinance institutions with a total asset value of $38.2 million loss to investors. The unprecedented commercial banks' failure in Ghana is ascribed to the impairment allowances to gross advances ratio (CDR) for the commercial banks which increased from a low of 6.6% in 2012 to a high of 7.9% in 2016 representing an average hike in the CDR rate by 6.4% in 5 years [3,4]. The commercial banks failure in Ghana between 2000–2008 represents an average banks failure rate of 12.5%, that is 1/8 banks x 100 =12.5%. The distressed commercial banks were Banks for Housing and Construction, Meridian BIAO Bank, Bank for Credit and Commerce International, Ghana Co-operative Bank, Capital Bank, Unique Trust Bank and Merchant Bank.

In August 2017 the Central Bank of Ghana revoked the operating licenses and closed down two major commercial banks for failure to meet the minimum capital requirement and also breached the corporate governance procedures. The banks were Capital Bank and Unique Trust Bank [13]. Failure of commercial banks has dreadful effect on the financial stability of the Ghanaian banking industry and the national economy at large as depositors undeservedly lost their money, more so, bank failure is not limited to commercial banks but also extended to rural banks and microfinance institutions.

In the same period (2000- 2008) the Central Bank closed down Tano Rural Bank, Tano Agya Rural Bank, City Savings and Loans Company, EquipSusu Microfinance, MFa Microfinance, Divine Microfinance and Emends Microfinance. In 2016, DKM one of the significant microfinance institutions was closed down by the Central Bank of Ghana with a net liability stood at ₵21 million. The Central Bank of Ghana revoked the operating license due to capital inadequacy, fraud and regulatory breach [3]. This phenomenon has remained as a shocker to the banking community in Ghana. The reasons adduced by the Governor of Bank of Ghana to close down commercial banks were ascribed to liquidity and capital challenges [3]. Likewise, the sudden collapse of Capital Bank and Unique Trust Bank was primarily due to banks failure to meet the regulatory minimum capital requirement and the deterioration in the capital adequacy ratio.

As a result, the Central Bank of Ghana appointed the Price Waterhouse & Coopers (PwC) to stand in a receivership position to liquidate the assets of the collapsed banks and distribute proceeds to pay off creditors and other secured liabilities (Bank of Ghana Report, 2017, PwC, 2017). Ghana Banking Survey (2017) indicated that the collapse of the two banks may be attributed to the energy sector loans of ₵11billion owed by Government of Ghana to UT Bank and Capital Bank. Nonetheless, others attributed the cause of failure to factors such as break down in corporate governance structures, credit default rate, capital adequacy ratio, lack of commercial banks know-how in information technology, high rates of corporation tax, increase in inflation and interest rates) [3].

Kusi, et al. [14] specified that modern government's taxation and other fiscal policies are considered predominant and ranked high amongst factors that cause commercial banks failure. The commercial bank's failure in Ghana has a bizarre consequence on the financial health of the domestic national economy-escalating the rate of inflation, interest and exchange rates increases exponentially, thereby, affecting banks performance [3]. The sudden collapse of commercial banks may cause investor cynicism and reduce the level of investment in the Ghanaian economy [8]. As noted by Appiah [11] and Samanhyia, et al. [3] commercial banks failure may create disincentive to savings, reduce investment in the productive sectors, creates mass unemployment and affects development and growth. The study of the factors that causes commercial banks failure is to help suggest appropriate measures to deal with such situations to forestall the problem of banks failure in Ghana.

This study follows the path of chosen by Samanhyia, et al. [3] and sought to identify the factors (corporate governance elements) that causes commercial banks failure in Ghana. An evaluation of the factors that causes banks failure would help outline policy recommendations to address those factors to make commercial banks more resilient and profitable. The study also seeks to contribute to the body of knowledge by providing understanding on factors that contributes to banks failure in emerging economy like Ghana.

Corporate governance vs. bank failure

Samanhyia, et al. [3] noted that analysis of corporate governance and corporate failure prediction studies between 1966- 2012 has not specified particular theoretical frameworks that need to be followed by future researchers who would want to conduct similar studies. The study indicated that future researchers who would want to conduct a study on the subject area need to concentrate on a specific theory which informs such an investigation instead of placing an over-reliance on the quantitative design. The absence of specific theoretical framework used to forecast corporate failure presents itself as an essential theoretical gap in the corporate governance and failure prediction model [11].

Platt and Platt [15] indicated that the theoretical frameworks that underpin corporate failure prediction models are available and contained in various studies on the subject around the world. A critical characteristic of the development of this theoretical framework is the requirement that returns on asset (ROE), the return on total assets (RoA) and the share of industry assets (SoIA) is an approximated measure and an indication of possible failure of commercial banks. The presumption is that a higher (RoE, RoA and SoIA) are indication that banks are sound and solvent. On the other hand, if RoE, RoA and SOIA are low that indicates that banks are likely to fail [3,11].

Samanhyia, et al. [3] and Wu, et al. [16] indicated that the relevant theoretical frameworks are non-existence on the subject and where they exist, they are mostly not connected to contemporary study. More so, the significance of the use of a quantitative design by a study is incredibly tricky for insolvency to be shelved by management especially when such an approach is employed [16]. In this regard, researchers might not be interested in concepts used to develop banks failure extrapolation plan but consider the quantitative outlook [17]. Nonetheless, it was suggested that potential researcher’s forthcoming should ponder about conceptual debates as the basis for the choice of appropriate economic and non-economic elements to build a robust quantitative research design [18]. However, the critical statistical methods or design used in prior studies include simple linear and multiple regression methods [11]. As a result, this study drew heavily on the strength of multiple regression approach to establish the relationship between governance variables and banks failure. More so, this study leveraged on the analytical instruments used in previous studies using panel data to achieve a validity and accuracy of the study.

Appiah [11] and Samanhyia, et al. [3] revelled that most of the past research designs used to examine the factors that causes commercial bank failure provided evidence that supports only the mathematical significance of the selected research variables ignoring the economic significance. Samanhyia, et al. [3] further indicated that the downside of the statistical design limits the meaningfulness of the current corporate failure prediction frameworks and this strongly emphasized that the essential factors that trigger failures are beyond scientific and economic realities. Apart from the mathematical and the economic significance of the research design used to examine commercial banks failure, the governing board structure and key elements are crucial to such an adventure [19].

Consequentially, there was a radical reform in the corporate governance legislation of the United States of America and United Kingdom. One of such essential reforms in the US was Sarbanes-Oxley's corporate governance Act of 2002 which fundamentally detailed out the corporate governance responsibilities bestowed on the management of commercial banks to secure the continued existence and profitability of registered commercial banks [11]. Similarly, in the UK was the Cadbury's corporate governance Act of 1992 that outlined essential recommendations to mitigate economic inconsistencies and, to develop governance arrangements that relate to the shareholders, boards and management of commercial banks to mitigate agency problems and to prevent banks failure [3]. In 1995, the House of Commons in the UK passed the Greenbury's corporate governance Act which demonstrated the need for distribution of executive obligations and payment of allowances to the governing board members [8]. The viewpoint of this Act was to ensure that there is equal payment of executive remunerations, avoid payment overruns to board members and to secure board accountability [19]. After the sudden demise of Baring Bank, the House of Commons tasked Hampel to propose a third corporate governance bill which was passed into an Act in 1998.

Contained in that Act, Hampel serialized and supported vital governance elements spontaneously contained in the Cadbury’s Act of 1992 and Greenbury’s Act of 1995. Hampel further, highlighted that board hugging and haggling will neither mitigate against financial misemployment nor promote commercial banks financial robustness and continuity [3].

In the United States of America, there were several corporate governance reforms and legislation that took place after the sudden collapse of (Enron Incorporation). Lessons learnt in the Enron's sudden demise generates massive debate amongst industry players and calls for reforms in the corporate governance arena [3]. This reform is expected to tighten the responsibilities of the outside executive directors on the governing boards increase their oversight responsibilities and to prevent the imminent collapse of commercial banks [19]. Platt and Platt [15] hinted that although there was limitation of knowledge about corporate governance reforms in the past, however, some prior studies employed the harmonized pared and wealth-enhancing techniques to estimate the effect of board attributes and the interconnections with other elements to predict banks failure.

Agrawal and Chadha [20] noted that superior governing board structure and appropriate mix of outside executives might mitigate renowned and classical commercial banks insolvency and increase the potential for survival and profitability. In this regard, commercial banks constituted by little board size and insufficient number of non-executives and outsized shareholding are susceptible to insolvency and subsequent failure.

Appiah [11] in a similar study found that insolvent commercial banks revealed poor board characteristics and structure in terms of oldness of the managing directors, senior management and the managing directors' participation in similar positions. Agrawal and Chadha [20] further indicated that unsuccessful commercial banks unveiled a large pool of dull and inexperienced governing board members. Contrary, Appiah [11] indicated that non-failed firms demonstrated greater size in structure in a mix of non-executive directors and female directors on the governing boards. Samanhyia, et al. [3] hinted that the deployment of the board elements in different studies produced evidence which limit a proper grasp of corporate governance variables such as the governing board size, mix of female executive’s directors and non- executive directors and failure of banks in Ghana.

In the Ghanaian context, Mahama [12], Soyode and Bande [21] have considered aspects of corporate governance variables that are quantitative and explains the reasons for banks failure. Charitou, et al. [19] and Soyode and Bande [21] used corporate governance variables such as the mix of female and non-executive directors to explain how these variables connect to explore answers to banks failure. This quantitative study would critically review the board size, blend between outside executive directors and the mix of female executive directors of the twenty-one (21) sampled commercial banks to assess the level of relationship and banks failure. Further, the quantitative study sought to identify the philosophical gaps and add to the exiting conceptual framework relating to exploring the relationship between corporate governance elements and banks failure.

Corporate governance

Appiah [8] saw corporate governance as a function to direct rather than control the activities of an enterprise. Corporate governance functions include running of a business, overseeing the executives' actions and satisfying litigate expectations of accountability.

Corporate governance is the structure, business processes, cultural settings and value systems of an enterprise [11]. More so, corporate governance is a set of procedures, standards, processes, laws and regulations which are used to direct and control the affairs of an entity [22]. The Ghanaian Securities and Exchange Commission also explain corporate governance as the ways by which corporate bodies are managed and directed [23]. Besides, the Organization for Economic Co-operation and Development (OECD) saw corporate governance as a set of relationships governing the various members of a corporation or a system by which business corporations are directed and controlled. This set out the distribution rights and responsibilities amongst the different participants in a corporation such as the board, managers, shareholders and other stakeholders while spelling out the rules and procedures for making decisions on corporate affairs [11]. To this end, corporate governance provides the structure through which the objectives are set and the means of attaining those objectives [24]. Due to lack of the existence of corporate governance frameworks in Ghana's economy, this study adopts the classical definition of corporate governance in the United Kingdom where Corporate Governance is seen as a system by which a firm is directed and controlled [19].

The quantitative study leveraged on corporate governance models such as Anglo– American model [25], Japanese model [23] and German model [26] as a foundation to explain the relationship between board elements such as total board size, mix of female directors and non- executive directors and how these board elements connect to banks-specific financial proxies to influence bank’s success or failure in Ghana.

Corporate governance models

In as much as, banks are the key players in the global economic environment and serves as the key driver of a country’s economic growth and helped to accelerate investment, it is pertinent to understand the relationship between the shareholders, investors, managers and to strike a balance between the varying interests to enhance banks performance [23,24]. In a bid to advance these varying interests and to accelerate development and growth, different countries across the world have developed corporate governance frameworks and models [8,25]. In addition, the corporate governance frameworks identify how investors control the manager's actions and how the responsibilities are divided between varying interested stakeholders that is owners and managers [20,27]. The corporate governance structure of jointstock corporations in a given country is determined by several factors including the legal and regulatory frameworks outlining the rights and responsibilities of all parties involved in the corporate governance debate, the de-facto realities of the corporate environment in the country and each corporation’s articles of association [27]. Modern researchers such as Agyemang, et al. [28], Ogege and Boloupremo [27], Chadha [29] have all identified three (3) models of corporate governance in developed capital markets namely the Anglo-American model, Japanese model and German Model. Therefore, this study is anchored on these corporate governance models and described the constituent elements and demonstrated how each model was developed in response to particular country-specific factors and situation. Besides, it is important to note that it is not very easy and simply to select a model and apply it to a given country like a blanket, instead, the process of selecting a model is dynamic and need to be developed in response to specific country conditions.

Anglo-American model

The Anglo- American model is characterized by share ownership of individual investors and institutional investors not related to the company also known as outside shareholders, as well, developed legal frameworks defining the rights and responsibilities of the three key players in the company’s affairs namely management, directors and shareholders. The Anglo-America model also defined comparatively and uncomplicated procedures for interaction between shareholders and corporations, as well as amongst shareholders during or outside the annual general meetings [25,28]. In the days old, corporate governance models are developed based on social, legal and economic conditions found in a particular country and those models vary in terms of a particular jurisdiction’s legal and reporting systems [23,30]. The Anglo-American model also sometimes called as an outside model is characterized by scarcity of capital and has the tendency to increase outside ownership which is not connected to the organization [24]. This model is synonymous to free- market economy orientation aimed towards capital formation with the objective to maximizing shareholder value [25]. As outside model, there is a large number of shareholdings with a negligible amount of share value and most importantly the decisions are made by the managers who are appointed to manage the resources of the company [25]. The Anglo- American model is characterized by the dominance of independent persons and individual shareholding and capital formation. As a result, the manager is responsible to the governing board of the company and shareholders and the latter being especially interested in profitable activities and received dividends from profitable investments [24]. It ensures the mobility of investments and their placement from the inefficient to the developed areas but it, however, feels a lack of strategic development.

In recent times, there is the ever-increasing influence of boards, investors increasing demand for higher returns and potentially risk-averse and managers give attention to important key business decisions to promote shareholder wealth [30]. The Anglo- American models, is developed within the context of the free-market economy and assumes the separation of ownership and control in most publicly held companies [25]. The important legal distinction serves as a valuable business and social purpose for investors to contribute capital and maintain ownership in the company whereas generally, avoiding legal liability for the acts of the corporation [25].

Investors avoid legal liability by ceding to management control of the corporation and paying management for acting as their agent by running the affairs of the company [23]. The cost of this separation of ownership and control is termed as agency costs. This means that the interest of shareholders and management may not always coincide, therefore, in many jurisdictions there are mediation laws governing enterprises based on the Anglo- American model attempting to reconcile this conflict in several ways [25]. Besides, they prescribe the election of a governing board of directors by shareholders and require that boards act as judiciaries for shareholders interest by overseeing management actions on behalf of shareholders [25].

Therefore, under this model organizations are required to fully disclose financial information compared to those organizations in Japan and German [30]. More so, corporations are expected under this model to balance the varying interest of stakeholders such as the shareholders, the governing boards and managers [20].

The bottom line here is that shareholders provide capital and required return on their investment and owned company, whereas the governing board is appointed by the shareholders to oversee the affairs of the company and the managers responsible for the day- to-day administration of the organization [30].

German Model

The German corporate governance model differs from both the Anglo- American and the Japanese models, although, some of its elements resemble the Japanese model. The German corporate governance model allows banks to hold long-term stakes in other corporations and as it is in the case of the Japanese corporate governance model, banks representatives are elected to corporation governing boards [28].

Mostepaniuk [25] stated that banks representation is consistent but unlike the Japanese model where banks representatives were elected to a corporation board only in times of financial distress situations, the German model allows three largest universal banks that provide a multiplicity of services in corporation’s management [25]. Besides, there are three unique features of the German model that distinguish it from the other models outlined in this study. Two of these elements has to do with the composition of the governing board and one concerns with shareholder rights and responsibilities [28].

Adegbite [24] and Mostepaniuk [25] indicated that the German model prescribes two boards with separate membership and that German enterprises have two-tiered board composition consisting of a management board (made-up entirely of insiders that is executive of the corporation) and a supervisory board (composed of employee representatives and shareholders representatives). The two boards are completely distinct and no one may serve simultaneously on a corporation's management board and supervisory board. Second, the size of the supervisory board is set by law and cannot be changed by shareholders. Mostepaniuk indicated that in Germany and other countries following these model-voting right restrictions apply and are legal and this may limit a shareholder to voting a certain percentage of the company's total share capital regardless of share ownership position. Mostepaniuk stated that most German corporations have traditionally preferred bank financing over equity financing, as a result, German stock market capitalization is small concerning the size of the German economy. Besides, the level of individual stock ownership in German is low and this reflects Germans' conservative investment strategy [26]. It is not surprising, therefore, that the corporate governance structure is geared towards preserving relationships between industry players notably (banks and corporations) [25]. The German model is somewhat ambivalent towards minority shareholders and allowing them to scope for interaction by permitting shareholder proposals also permitting companies to impose voting rights restrictions. The percentage of foreign ownership of German equity is significant in 1990, however, it was 19 percent [26]. This ratio is slowing down and beginning to affect the German model as foreign investors from inside and outside the European Union begin to advocate for the payment of their interests. More so, the effect of globalization of the capital markets is forcing German corporations to change their corporate governance model to be investor friendly [26].

Besides, the Japanese and German models are best described as insider models as the ownership rights are distributed amongst insider interests which are somehow connected to the organization and own a relatively larger amount of share capital [23,25]. As a result, the relationship between interested parties of the company is extremely important and the objective of the insider model is not only to maximize investors return but also to maximize the welfare of other stakeholders [26]. Besides, based on the German model organizations are seen as the combination of various interest groups aimed to coordinate the national interest objectives, that is to promote economic development and growth, for example, in the days old, German banks played an important role in corporate decisions that helps to accelerate economic development and growth [26]. Under this model, a great deal of importance is given to the protection of creditors even to the point where a bank might dominate a firm. Further to this, it ensures the depositary voting right to control the decisions and votes in a company [25,30]. The German system of corporate governance is dual function aimed at coordinating national policy to provide employees access to information and participation in various activities of the organization and to promote industrial democracy [25,26]. As a matter of corporate governance rules, within any bank, there is an executive board and a supervisory council and the executive board effectively manage the organization, but under the direction of the latter and most decisions are necessarily confirmed by it and such a governance structure is a mechanism for management monitoring and control.

Japanese model

The Japanese model of corporate governance uses a different dimension called the holding concepts. This concept designates industrial groups consisting of companies with common interests and similar strategies [31]. The managers' role manifests itself in relation with shareholders and keiretsu. Keiretsu is a network of royal suppliers and customers. Keiretsu represents a complex pattern of a corporation and also competitive relationships characterized by the adoption of defensive tactics in hostile takeovers thereby reducing the degree of opportunism of parties involved and keeping long term business relationships. Most Japanese banks are affiliated with this group of trading partners and the characteristic pattern of governance is dominated by two types of legal relationships. The first group is one of codetermination between shareholders, unions, customers, suppliers, creditors and government [25,31]. The second group is made up of a ratio between administrators and those stakeholders including managers. The necessity of the model results from the fact that the activity of a company should not be distressed by the relations between all these people. Management decisions pursue improvement in the income and power of an enterprise, in particular by specific corporate practices though; sometimes the shareholders' control of the management can be hampered [31]. In spite of this the Japanese model is similar to the German model since both systems are based on internal control systems and it does not focus on the influence of strong capital markets but the existence of those strategic shareholders such as banks [30]. As in Germany, major shareholders are actively involved in the management process to stimulate economic efficiency and to penalize its absence. It also aimed at harmonizing the interests of social partners and employees of the entity.

The Japanese governance systems facilitate the monitoring and flexible financing of enterprise, effective communication between the banks, as the main source of financing consists of bank loans [26]. In addition, the owners of corporations are other companies or even banks which control the management strategies; ownership is always oriented towards control, justifying the limited issues of shares. Besides, most ownership of banks are held by fix shareholders who can also be major suppliers, creditors, customers to maintain long term relationships of trust and to obtain again. From the forgone discussions, it is evident that corporate governance models sought to establish the relationship between management of companies, stakeholders and society at large. This is aimed at promoting fairness, transparency and accountability concerning the various legal frameworks that are used to govern and to ensure that actions of managers are taken with due regards to the interests of key stakeholder groups aimed at increasing profitability of banks [26].

Based on the above, this study is anchored on the Anglo-American corporate governance model which sought to establish a relationship between the various interest groups of the company and to define ways to manage any possible conflicts that may arise from such as a relationship aimed to increase profitability and to make commercial banks resilient.

Conceptual framework of the study

The conceptual framework shown in Figure 1 explains the linkages between corporate governance elements as well as other control factors and bank performance.

Figure 1. Conceptual framework of corporate governance on banks performance.

The conceptual framework in Figure 1 shows that corporate governance elements can positively affect banks performance by improving accountability amongst managers, advice on business strategy and access to external capital. In addition, the negative effects of corporate governance on profitability can occur through implementation costs, free-rider problem and regulation among others [32,3].

Random sampling/data standardisation

The study randomly sampled 21 registered commercial banks. This was estimated based on the Ghana banking survey conducted by Price Water House and Coopers (PwC) in 2017. Contained in that report the average performances of registered commercial banks with variance for the year 2016 are stated below:

ROE = 0.12 ± 0.16%, ROA = 0.02 ± 0.03%, SOIA = 0.04 ± 0.03%

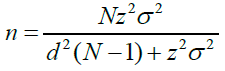

Based on this result, the study estimated the sample using the finite population of banks with published financial statements of 28 banks. Seven (7) banks at the date of the report did not have complete and authentic financial statements and were thus excluded from the sample space. The performance indicator which gave the maximum possible sample size (ROE) was adopted for this study. The sample was standardized using the formula of sampling for a finite population as stated below with assumptions:

N = 28, σ2 = 0.02649, z = 1.96, d = 0.04

From the sampling frame of 28 banks the study randomly selected the 21 banks whose data were used in answering the stated research questions.

Data source

The annual report and published financial statement of the 21 selected banks between (2012 – 2016) was obtained from the Bank of Ghana, the Banking Supervision Department and the Ghana Banking Survey conducted by Price Waterhouse and Coopers (PwC) in 2017.

Prior to data collection, the researcher sought a formal permission from the Head of the Banking Supervision Department of the Bank of Ghana and the Head of the Customer Service Department of PwC to access its database for annual report and published financial information on the 21 sampled banks. The data was further processed using Mat lap to generate key financial proxies and corporate government variables. Banks with incomplete and inadequate corporate governance and financial information were removed from the dataset for analysis purposes.

Data analysis

At the onset of data analysis, the balance of the panel data was tested. Key descriptive statistics for the data set was computed consisting of the mean, standard deviation, minimum and maximum and values were also generated for each dependent and independent variable. A correlation test was conducted to establish the relationship between bank performance proxies and corporate governance factors as well as the control variables. Finally, the relationship between corporate governance variables on banks RoE, RoA and SoIA was estimated using the random effect models as specified in the equations in the study. The quantitative study employed random effect panel data estimation techniques to estimate the effects of corporate governance elements on bank’s performance. The model assumes that variations across banks are random and uncorrelated with the independent variables included in the model [3,11]. The study specifies the random effect models as follows:

Where α0,β0,δ0 are the intercepts; αnit,βnit,δnit are the coefficients and εit is the error term. A summary description of the variables in the model is shown in Table 1.

| Variables | Measurement in Percentages (%) |

Apriori Expectation |

|---|---|---|

| Failure Proxies | ||

| ROEit | Return On Equity (ROE) | - |

| ROAit | Return On Assets (ROA) | - |

| SoIAit | Share of Industry Assets (SoIA) | - |

| Governance Variables | ||

| X1it | Total Governing Board Size (TGBS) | +/- |

| X2it | Female Executive Directors (MOFED) | +/- |

| X3it | Non-Executive Directors (MONED) | +/- |

| Control Variables | ||

| X4it | Credit default rate (CDR) | - |

| X5it | Capital adequacy ratio (CAR) | + |

| X6it | Liquidity ratio (CACL) | + |

| X7it | Inflation (IFL) | - |

| X8it | Taxation (TAX) | - |

| X9it | Gross Domestic Product (GDP) | + |

Descriptive statistics

The variables used in the study include the dependent variables (RoE, RoA and SoIA) and the independent variables corporate governance elements (TBS, MOFED and MONED); and control variables (CDR, CAR, CACL, IFL, TAX and GDP) (Table 2).

| Variables | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| ROE | 0.20 | 0.14 | -0.06 | 0.51 |

| ROA | 0.03 | 0.02 | -0.03 | 0.09 |

| SoIA | 0.05 | 0.03 | 0.00 | 0.15 |

| TGBS | 9.52 | 1.98 | 6.00 | 13.00 |

| MOFED | 2.00 | 1.75 | 1.00 | 7.00 |

| MONED | 7.81 | 1.98 | 4.00 | 11.00 |

| CDR | 0.07 | 0.06 | 0.00 | 0.26 |

| CAR | 0.19 | 0.45 | 0.00 | 4.53 |

| CACL | 0.65 | 0.28 | 0.00 | 2.00 |

| IFL | 0.13 | 0.01 | 0.12 | 0.14 |

| TAX | 0.33 | 0.34 | 0.00 | 1.29 |

| GDP | 0.12 | 0.01 | 0.11 | 0.14 |

From Table 2 the mean of RoE is 2% with a standard deviation of 1.4% implying that RoE is not widely dispersed around its average. This suggests that return on investor's equity in the Ghanaian banking industry has relatively been stable between the periods 2012 to 2016. Further to this, evidence from the summary statistics indicated that the mean of RoA is 0.3% with a standard deviation of 0.2% implying also that RoA is not widely dispersed around its average. The results in Table 2 found that the mean of SoIA is 0.5% with a standard deviation of 0.3% indicating that there is a narrow dispersion of SoIA around its average. This also implies that the share of industry assets of Ghanaian banks has been stable within the periods of study (2012 - 2016).

With regards to corporate governance indicators, average board size was found to be around 9 or 10 with a standard deviation of about 1.98, implying that considering the period between 2012 to 2016, Ghanaian banks had relatively similar board sizes. Furthermore, it is obvious from the study that the average number of female executive board members was 2 with a standard deviation of about 1.75, indicating that with the period 2012 to 2016, Ghanaian banks had relatively similar gender diversity in the boardrooms. Results from Table 2 revealed that the average number of non-executive board members was about 8 with a standard deviation of about 1.98 which also suggests that within the period 2012 to 2016, Ghanaian banks had a similar fair representation of non-executive members on the boardrooms. CDR was 0.7% with a standard deviation of about 0.6, which suggest that Ghanaian banks were able to maintain relatively low credit default rate over the period 2012 to 2016.

CAR was 19% with a standard deviation of about 45%, which implies that the adjusted equity to risk-adjusted asset base as required by the Bank of Ghana (BoG) was widely dispersed within the period 2012 to 2016 among Ghanaian banks. CACL had a mean of 65% with a standard deviation of about 28%, which indicates that the banking sector was able to achieve the statutory liquidity requirement of 20% of deposits and short-term liabilities. Nonetheless, there is a vast variation in the level of liquidity among banks in Ghana. IFR during this period was relatively low as 12% and peak at 14% and averaged 13% with a standard deviation of 0.1%. TAX had a mean 33% and a standard deviation of 34% and had a minimum and a maximum of 0 and 1.29 correspondingly. The GDP within the 5 years averaged 12% with a standard deviation of 01% varying between 11% and 14% respectively.

Normality (Multi-collinearity test)

Adekola (2016) and Wijekoon and Azeez (2015) hinted that the VIF tolerance test is a variance analysis detecting the presence of multicollinearity amongst the independent variables. Table 3 shows a summary of the VIF tolerance level for each of the independent variables.

| Variables | VIF | 1/VIF |

|---|---|---|

| GDP | 6.95 | 0.143819 |

| TAX | 6.3 | 0.158848 |

| MONED | 5.1 | 0.196052 |

| TGBS | 4.26 | 0.234871 |

| IFL | 2.34 | 0.427907 |

| MOFEB | 2.09 | 0.477792 |

| CAR | 1.32 | 0.756381 |

| CACL | 1.31 | 0.763057 |

| CDR | 1.06 | 0.939686 |

| Mean VIF | 3.41 | - |

From the summary of the VIF tolerance for the independent variables, it can be observed that given the magnitude of the VIF levels none of the independent variables is highly correlated with another. The statistics show that the standard deviations of the data set are normally distributed. The correlation coefficients (lower and upper) are within relevant range with the VIF.

Correlation analysis

Abor [33] and Chadha [29] argued that a correlation above 0.8 between independent variables should be corrected for multicollinearity. When a variable has a co- efficient equal to or greater than 0.8 it is near perfect or highly correlated. From the correlation matrix, none of the variables is highly correlated with another.

Correlation analysis for return on equity (RoE)

Table 4 presents the correlation results for Return on Equity (RoE) and the corporate governance indicators as well as both the internal and external control variables considered in this study.

| Variables | ROE | TGBS | MOFED | MONED | CDR | CAR | CACL | IFL | TAX | GDP |

|---|---|---|---|---|---|---|---|---|---|---|

| ROE | 1.10 | |||||||||

| TGBS | 0.10 | 1.00 | ||||||||

| MOFED | 0.37*** | -0.18 | 1.00 | |||||||

| MONED | -0.14 | -0.12 | -0.50*** | 1.00 | ||||||

| CDR | -0.12 | 0.04 | -0.03 | -0.12 | 1.00 | |||||

| CAR | -0.30** | -0.02 | 0.03 | -0.10 | -0.11 | 1.00 | ||||

| CACL | 0.14 | -0.27* | 0.06 | 0.02 | 0.15 | -0.19 | 1.00 | |||

| IFL | -0.00 | -0.00 | -0.00 | 0.00 | 0.07 | -0.04 | 0.06 | 1.00 | ||

| TAX | -0.03 | -0.08 | -0.02 | -0.01 | 0.00 | 0.24* | 0.16 | -0.17 | 1.00 | |

| GDP | 0.05 | -0.00 | 0.00 | 0.00 | -0.02 | -0.06 | -0.06 | -0.28** | -0.79*** | 1.00 |

From the correlation result in Table 4 the total governing board size (TGBS) has a positive and weak correlation with RoE with a correlation coefficient of 0.10. This implies that in a descriptive sense, RoE has a very weak association with total governing board size. Also, board gender diversity (MOFED) has a significant positive correlation with the RoE with a correlation coefficient of about 0.37. This implies that descriptively, board gender diversity has a moderately strong correlation with the RoE. Furthermore, it is evident from table 4 that MONED has a negative and weak correlation with the RoE with a correlation coefficient of 0.14. This implies that in a descriptive view, there is a negative, weak and insignificant association with RoE. There is a negative correlation between RoE and all internal and external control variables except for Liquidity Ratio (CACL). The relationship between Capital Adequacy Ratio (CAR) and RoE was statistically significant. This implies that from a descriptive point of view, Credit Default Rate (CDR), Capital Adequacy Ratio (CAR), Taxation (TAX) and the Gross Domestic Product (GDP) and Inflation with exception of liquidity Ratio, exhibited a negative association with RoE. Thus, the study fails to reject the null hypotheses that TGBS, MONED, CDR, CACL, GDP, TAX and IFL has no relationship with RoE. The study rejects the null hypothesis of no association between MOFED and CAR and RoE and accept the alternate hypothesis that a relationship exists.

Correlation analysis for return on assets (RoA)

Table 5 presents the correlation results for Return on Assets (RoA) and the corporate governance indicators and the internal and external control variables considered in this quantitative study.

| Variables | ROA | TGBS | MOFED | MONED | CDR | CAR | CACL | IFL | TAX | GDP |

|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 1.00 | |||||||||

| TGBS | 0.06 | 1.00 | ||||||||

| MOFED | -0.17 | -0.18 | 1.00 | |||||||

| MONED | -0.02 | -0.12 | -0.50*** | 1.00 | ||||||

| CDR | 0.10 | 0.04 | -0.03 | -0.12 | 1.00 | |||||

| CAR | -0.28** | -0.02 | 0.03 | -0.10 | -0.11 | 1.00 | ||||

| CACL | 0.06 | -0.27* | 0.06 | 0.02 | 0.15 | -0.19 | 1.00 | |||

| IFL | -0.01 | -0.00 | -0.00 | 0.00 | 0.07 | -0.04 | 0.06 | 1.00 | ||

| TAX | -0.06 | -0.08 | -0.02 | -0.01 | 0.00 | 0.24* | 0.16 | -0.17 | 1.00 | |

| GDP | 0.01 | -0.00 | 0.00 | 0.00 | -0.02 | -0.06 | -0.06 | -0.28** | -0.79*** | 1.00 |

From the correlation result in Table 5 above TGBS has a positive and weak correlation with the RoA and with a correlation coefficient of 0.06. In a descriptive sense RoA exhibited a positive but very weak association with the TGBS. Also, MONED has a negative and a very weak correlation with the RoA with a correlation coefficient of about 0.03. This implies that descriptively, presence of non-executive directors on the board of commercial banks exhibited a positive but weak association with the RoA. It is evident from Table 5 that board gender diversity MOFED has a negative and a weak correlation with the RoA with a correlation coefficient of 0.17. This implies that there is a negative, weak and insignificant association with the RoA. There are negative correlations between RoA and some of the internal and external control variables that is CAR, IFL and TAX. The relationship between CAR and RoA was statistically significant at 1%. However, there are positive correlations between RoA and other internal and external control variables including CDR, CACL and GDP. This implies that from a descriptive point of view, Capital Adequacy Ratio (CAR); Taxation (TAX) and inflation (IFL) except for Credit Default Rate (CDR), Liquidity (CACL) and the Gross Domestic Product (GDP), exhibited a negative association with RoA.

Correlation analysis for share of industry assets (SoIA)

Table 6 presents the correlation results for Share on Industry Assets (SoIA) and the corporate governance indicators as well as both internal and external control variables considered in this study.

| Variable | SoIA | TGBS | MOFEB | MONED | CDR | CAR | CACL | IFL | TAX | GDP |

|---|---|---|---|---|---|---|---|---|---|---|

| SoIA | 1.00 | |||||||||

| TGBS | 0.20* | 1.00 | ||||||||

| MOFED | -0.05 | -0.18 | 1.00 | |||||||

| MONED | -0.18 | -0.12 | -0.50*** | 1.00 | ||||||

| CDR | 0.18 | 0.04 | -0.03 | -0.12 | 1.00 | |||||

| CAR | -0.17 | -0.02 | 0.03 | -0.10 | -0.11 | 1.00 | ||||

| CACL | 0.08 | -0.27** | 0.06 | 0.02 | 0.15 | -0.19 | 1.00 | |||

| IFL | 0.00 | -0.00 | -0.00 | 0.00 | 0.07 | -0.04 | 0.06 | 1.00 | ||

| TAX | -0.02 | -0.08 | -0.02 | -0.01 | 0.00 | 0.24* | 0.16 | -0.17 | 1.00 | |

| GDP | -0.00 | -0.00 | 0.00 | 0.00 | -0.02 | -0.06 | -0.06 | -0.28** | -0.79*** | 1.00 |

From the correlation result in Table 6 above, only the TGBS has a positive and significant relationship with SoIA with the highest correlation coefficient of 0.20. This implies that in a descriptive sense, SoIA exhibited a positive but very weak association with corporate governance variable (TGBS). The MOFED and MONED had negative and weak relationships with SoIA. These relationships, however, were not statistically significant.

There are positive but weak correlations between SoIA and all the internal and external control factors except for Capital Adequacy Ratio (CAR), Gross Domestic Product (GDP) and Taxation (TAX), which had negative and weak correlations with SoIA. This implies that from a descriptive point of view, all control factors except for CAR, GDP and TAX, exhibited a positive but weak association with the SoIA. The study fails to reject the null hypotheses of no relationship between corporate governance structures, bank-specific financial indicators and macroeconomic indicators (MONED, MOFED) and the bank's SoIA. The study rejects the null hypothesis of no relationship between TGBS and the SoIA.

Random effect regression results

The random effect model was used to estimate the relationship between corporate governance variables, banks specific financial indicators and macroeconomic indicators and banks' failure or bank performance that is, return on Equity, Return on Assets and Share of Industry Assets. The results are presented in Table 7.

| ROE | ROA | SoIA | ||||

|---|---|---|---|---|---|---|

| Variables | Coefficient | Standard error | Coefficient | Standard error | Coefficient | Standard error |

| Constant | -0.012 | 0.421 | 0.065 | 0.081 | 0.035 | 0.074 |

| Corporate Governance | ||||||

| TGBS | -0.008 | 0.022 | 0.004 | 0.004 | 0.009 | 0.008 |

| MOFED | 0.040* | 0.017 | -0.004 | 0.003 | -0.003 | 0.006 |

| MONED | 0.020 | 0.024 | -0.004 | 0.005 | -0.008 | 0.008 |

| Control Variables | ||||||

| CDR | -0.519** | 0.182 | 0.011 | 0.035 | -0.015 | 0.029 |

| CAR | -0.033 | 0.022 | -0.007 | 0.004 | -0.001 | 0.003 |

| CACL | 0.047 | 0.044 | -0.013 | 0.008 | -0.008 | 0.007 |

| IFL | 0.322 | 1.516 | -0.069 | 0.289 | 0.021 | 0.231 |

| TAX | 0.031 | 0.061 | -0.001 | 0.012 | -0.001 | 0.009 |

| GDP | 0.114 | 1.686 | -0.060 | 0.322 | -0.037 | 0.259 |

| Wald Chi-square | 18.60* | 5.35 | 3.48 | |||

| Prob > Chi-square | 0.029 | 0.803 | 0.942 | |||

| R2 | 0.248 | 0.065 | 0.061 | |||

| Sigma_u | 0.086 | 0.018 | 0.034 | |||

| Sigma_e | 0.069 | 0.014 | 0.011 | |||

| Observations | 105 | 105 | 105 | |||

| Number of panel | 21 | 21 | 21 | |||

The results contained in Table 7 is summarised in a regression models 1, 2 and 3 below:

Based on the result of regression model 1, the coefficient of the MOFED and CDR are significant at the 5% significant level implying that gender diversity and credit default rate do matter in assessing the financial health of commercial banks in Ghana. Therefore, the model 1 was statistically significant at 5% (R2 = 0.25).

Based on the results produced by the random effect model, it is found that the coefficient of female representation (MOFED) is positive and statistically significant at 5% level of testing. This implies that a unit increase in the number of female executive directors on the governance board of commercial banks increases RoE by 4%. This result is consistent with the research findings by Appiah [11], Adegbite [24], Mostepaniuk [25], Samanhyia, et al. [3]. Therefore, at the 1% significance level the study accepts the alternate hypothesis H1a: there is a relationship between the mix of female executive (MOFED) and the RoE of banks in Ghana.

On the other hand, in terms of the banks-specific financial proxy, credit default rate (CDR) is negative and statistically significant at 1% level of testing. This implies that a percentage increase in credit default rate (CDR) significantly reduces RoE (or increases the likelihood of banks failure) by 51.9%. This result supports prior study by Abor [33], Amediku [1], Agyemang, et al. [28]. Hence, at the 5% significance level the study accepts the alternate hypothesis H2a: there is a relationship between credit default (CDR) and the RoE of banks in Ghana.

The empirical evidence from the quantitative study indicates a positive relationship between corporate government elements and banks failure in Ghana. This finding supports the objectives of the study. The study recommends that Bank of Ghana should develop a corporate governance framework to effectively increase the number of female executive representations (MOFED) on the governing boards. A balanced governing board should have six female executive directors to enhance gender diversity. This policy recommendation is to (a) enhance multiplicity of skills, (b) promote effective control and (c) improve financial performance.

In addition, commercial banks are required to develop effective systems for the management of banks-specific financial proxy, credit default rate (CDR) to boost financial soundness and profitability of banks in Ghana. In the case of managing credit default rate, three key policy measures are outlined (a) banks may set a threshold for granting of credit to customers, (b) board approval is required for a higher threshold of credit and (c) banks may use credit default swap to mitigate credit losses.

For future research, this study can be extended to cover unlisted commercial banks in Ghana whiles applying other econometric techniques to verify the effects. Researchers conducting a mixed study in the future may consider the cultural and ethical dimensions of Corporate Governance to help assess in whole the impact of the qualitative and quantitative dimensions on the study.