Research Article - (2021) Volume 10, Issue 11

Received: 01-Nov-2021

Published:

22-Nov-2021

Citation: Orina, Charles and Fred Sporta “The Effect of Mobile

Banking Loans on Operational Efficiency of Commercial Banks in Kenya”.

Int J Econ Manag Sci 10 (2021): 613.

Copyright: © 2021 Orina C, et al. This is an open-access article distributed under

the terms of the creative commons attribution license which permits unrestricted

use, distribution and reproduction in any medium, provided the original author

and source are credited.

The main objective of this study is to determine mobile banking effects on commercial banks’ operational efficiency. The study looked at mobile banking loans concerning commercial banks operational efficiencies in Kenya. The study was guided by the financial deepening theory. The study adopted a descriptive research design targeting 41 commercial banks in Kenya. The study adopted a census survey, using secondary data from Kenya's central bank and the commercial banks' annual financial reports in Kenya. Data on the number of loans and advances issued by the banks. The study covered nine years from 2010-2018. STATA software was used in data analysis, descriptive and statistical inferential. The independent variable was measured against the dependent variable to examine if they affected commercial banks' operational efficiency. Regression equations estimated the relationship between the variables. Hausman test was used to specify the adoption of random effect or fixed effect models in panel data. The Hausman tested and fixed effect model was selected. The diagnostic tests covering heteroscedasticity, autocorrelation, multicollinearity, and normality tests were also conducted. The findings were presented using graphs and tables. The results were as follows: Mobile loans (β=0.474, p<0.05). The study concluded that mobile banking loans had a significant effect on commercial banks' operational efficiency in Kenya. The study recommended that commercial banks invest more in mobile loans since it had a positive relationship with commercial banks' operational efficiency in Kenya. The study results would enhance the adoption of more financial innovation in the banking industry that would contribute to the economy's overall grow.

Mobile banking loans • Operational efficiency • Hausman test • Financial innovation

Due to the development of technology, especially in the telecommunication sector, mobile phone devices that have been used mainly for communication are now used to provide portable internet and electronic financial services like mobile loans, account opening, deposit and withdrawal. The focal point has been using this financial innovation to bring onboard the unbanked and those who have limited or no or limited access to financial services. Innovations in the industry, such as mobile banking, have aided the facilitation of this condition [1]. The Commercial Bank of Africa (CBA) developed a mobile loan product in partnership with Safaricom, replicating them in other African countries [2]. In 2014, the Commercial Bank of Africa (CBA) partnered with Vodacom in Tanzania to start M-Pawa services, a replica of M-Shwari. Then, the CBA Bank teamed up with MTN in Uganda to develop and customize the Mo Kash services for Uganda and Rwanda in 2017, and eventually the bank to bank partnership in Côte d'Ivoire to create the Mo Kash mobile service via a partner bank in Côte d'Ivoire in the year 2018, these have experienced tremendous growth in mobile banking services in these countries hence bringing financial inclusion and deepening into reality to their customers. In Kenya, according to the CAK first report of the 2019/2020 financial year, the active mobile money subscriptions are 31.2 million. The number of agents is 235,168. The number of transactions was 661.6 million for (withdrawals and sending) valued over KSh.1.7 trillion made [3]. In Kenya, mobile network operators like Safaricom introduced the mobile money service M-Pesa in 2007, and immediately became popular, drastically changing and increasing Kenyans' access to financial services. Safaricom's M-Pesa and other mobile money transfer platforms have to give a new commercial bank innovation phase in electronic banking. A classic example is a competition over a mobile platform, like the Equitel mobile product by Equity Bank. Collaboration between commercial banks and Mobile Network Operators (MNO) in the provision of mobile financial services has become a possibility like the case of CBA's M-Shwari and Fuliza, KCB M-Pesa, Equity's Eazzy pay, and Family bank Pesapap. The introduction of agency banking like cooperative banks' Coop Kwa Jirani and other commercial banks, mobile agency banking, Microfinance institutions, and mobile banking products. It has also led to Industry coordination using platforms such as the Pesa Link that offer money transfer alternatives. Pesa Link enables the transfer of money or payments by members of a particular bank to another using their mobile phone [4]. All these financial innovations enable service providers to deliver quality services to their customers.

Growth performance

The primary goal for any business organization is to grow. Different parameters in the banking sector can measure growth. Commercial banks' growth can be looked at geographical on the number of branches or the bank's presence in all the places. Banks increase mobile money transfers, mobile loans/credit, bank transactions, and bank accounts [5]. They noted that they are growing from 2014 to 2015 as indicated in their study on electronic banking and financial performance of commercial Banks in Kenya (CBK), which leads to an increase in mobile transaction fees, other charges, and commissions bank advance loans [6,7]. All these financial innovations will lead to commercial banks' growth in profitability, and profit growth can lead to reserve growth and equity growth. The commercial banks are undergoing financial innovation modifications due to the changes in information technology and telecommunication money transfer platforms. The changes have brought about the need for commercial banks to look for ways to operate effectively and efficiently by reducing their operational cost while maximizing their profits through the leverage of electronic banking like mobile, internet banking, and agency banking. Operational efficiency is the main goal for financial institutions or organizations. Managers can use strategies like promoting operational optimization and using technology to ensure that they operate efficiently [5].

According to a study done by Kamau and Oluoch, there is a significant positive relationship between ROE and the use of mobile banking services by commercial banks' performance. Another study on the effect of transferable credit on operational efficiency in Commercial Banks in Kenya (CBK) found that mobile banking has a desirable impact on commercial banks' performance, which is an attribute of the credit services offered using different channels like mobile loans [5]. Operational changes are achieved by automating many processes, reducing operating expenses, reducing paperwork, bank are using artificial intelligence and data analytics to predict customer behavior, and developing products depending on the customer ecosystem. Commercial banks offer mobile banking services like mobile banking loans, funds transfer, and saving products at low cost, while maximizing revenue on commissions. By introducing new products like CBA M-Shwari product, KCB M-Pesa, these products reduce operational costs by reducing processing time, queuing time, travel, transaction, office cost while offering fast, convenient, reliable services to their bank customers [4].

Statement of the problem

The financial services ecosystem has changed not only in Kenya but the whole world because of the revolution in computer technology. The current commercial banking industry is faced with stiff competition by financial providers and other non-bank financial services like fintech firms and MNOs [8]. As per the CBK annual report for 2018, the banking industry was forecast to remain resilient in 2019. With the various innovations like internet banking, mobile banking, and banks need to review their financial delivery channel and business models [9]. Mobile network operators have introduced appealing financial products like a mobile loan [10].

The emergence of digital financial innovators in the finance sector can pose a significant threat to the ancient retail banking model [11]. This innovation has led to collaboration with MNO like KCB mobile loans, MCoop loans by Cooperative Bank of Kenya, M-Shwari, for CBA, Eazzy loan, for Equity bank, Timiza for Barclays and HF Whizz for housing finance, and many other [12].

The banking industry is drastically changing due to commercial banks' financial innovations, like the recent financial report for the year 2017/2018 statements. It is a clear indication that mobile banking innovation are providing convenience, cost-effective, reliable and customer satisfaction services at a reduced cost leading to banks operational efficiency in Kenya hence attracting more customers and more mobile deposits and loans issued according to the Central Bank of Kenya annual report [13].

Some studies have been done on the effects of mobile banking on commercial banks' operational efficiency. The mobile credit improves operational efficiency in loan collection and commercial banks' general operational efficiency [4]. This study was specifically on mobile bank credit and not mobile banking. Looked at mobile banking's effect on commercial banks' performance and established no significant relationship between mobile banking and commercial bank performance in Kenya [14]. Mobile banking indicated a spike in the number of transactions in the year 2010 to 2019. Nigeria's banks' operational efficiency improved because of electronic banking compared to the traditional banking business [7]. The study concluded that the internet and mobile banking are statistically insignificant in Nigeria's operational efficiency concluded that mobile banking and agency banking positively affect mobile banking in Rwanda [15]. Due to these mixed findings, the researcher will like to investigate if mobile banking affects commercial banks' operational Efficiency in Kenya, which has not been studied by many scholars. Most studies have been done on mobile banking's effect on commercial banks' performance but not on operational efficiency and commercial banks’ mobile banking.

Past studies have produced mixed results. Some conclude that mobile banking financial innovation has some least effect on commercial bank operations, indicating a remarkable contribution to bank operations. It is at the center of such mixed conclusions that it creates and entails the need to carry out a study from a Kenyan perspective to examine mobile banking loans effect on commercial banks' operational efficiency in Kenya. Most commercial banks have introduced these financial innovations. They have invested in the digital innovation strategy to remain competent, and improve their operational efficiency. Will these innovations like mobile loans have any effect on commercial banks' operational efficiency?

Objective of the study

To establish the effect of mobile banking on the commercial bank's operational efficiency in Kenya. The specific objective to determine the effect of mobile banking loans on the operational efficiency of commercial banks in Kenya.

Research hypothesis

There is no significant relationship between mobile banking loans and commercial banks' operational efficiency in Kenya.

Theoretical review

The study will be guided by the financial deepening theory. The theory of financial deepening was formulated and developed, and it explains the role played by accessibility to credit on the firm's performance. The theory is premised because financial deepening is a necessary pre-condition for any economy's growth. The method is further premised because financial deepening ensures that credit is available to firms to finance the operations. The theory indicates that sound and efficient commercial sectors result in increased liquidity and mobilization of savings.

In support of these views, indicates that access to credit facilities is a valuable service offered by financial institutions. Since some small businesses are constrained from accessing a large amount of credit from larger financial institutions, mobile banking comes in to bridge the gap by availing customized credit facilities to clients, including small firms. The credit is used for, among other things, expansion of business operations and coming up with projects that generate revenues for the firm. Accessibility to credit facilities has also been associated with increased social protection and production potential. The theory informs how the adoption of mobile banking has enabled customers to access credit facilities. In return, this increases mobile transaction revenue, many registered mobile users, and the amount of money moved using mobile banking brings customer satisfaction and banking efficiency.

Empirical review

Mobile banking loans and operational efficiency in the study on fintech and banks collaboration: Does it influence the efficiency in the banking. The study objective was to establish the influence of fintech on banks' loan allocation ability using Data Development Model (DDM). Secondary data is from 2009-2018. The study noted a positive effect on the technical efficiency, which observed liquidity ratios, cost of income return on assets, and loan intensity. On the other side, the cost of intermediation and credit risk negatively affected technical efficiency. The study noted that depending on the inputs and the model adopted. Some factors like mobile banking, credit, digital account operations, which lead to the growth of bank accounts, increase in revenue generated by banks through commission’s charges on the services they are offering, increase the bank's technical and operational efficiency on the credit allocation. Still, the study concluded that collaboration between banks and fintech does not significantly affect the banking industry's efficiency. The research examined the influence of fintech and banks' collaboration on commercial banks' efficiency, which was not significant and mainly focused on loans. In contrast, this study will be focused on the effect of banking on commercial banks' efficiency.

The partnership strategy between commercial banks and mobile network operators offers digital mobile banking products, services, and processes. A good example is cooperation between the Commercial Bank of Africa and Safaricom. They developed a mobile loan application product called M-Shwari. According to the study, it was noted that when CBA bank partnered with M-Pesa, the banks have increased the number of customer accounts, deposits, and loans. It was indicated that the bank is offering a vast array of products, services, and processes like balance inquiry, interbank transfers, interest loans, mini-statement requests, interest on deposit savings lock account. M-Shwari product was introduced in the year 2012. It has been a single contributor to the bank's growth. The customers have perceived the product to be convenient, easy to use, secure, and cost less because the cost of withdrawal from an M-Shwari account to M-Pesa is free. Customers can request loans at the click of a button, which does not require paperwork and any guarantor as the traditional banks do. The account opening, loan request, account balance, and loan limit check are automated. This study reviewed the commercial bank of Africa products and services and not all the 41 commercial banks in Kenya, which this study intends to investigate.

In the success story of the Commercial Bank of Africa (CBA) of M-Shwari, it attained remarkable growth on the initial day of its operation by opening 70000 accounts, with an average of 32000 customers each day, within the next three months. In Kenya, for instance, the bank disburses mobile loans of 60000-70000 on average every day and 90000 during promotions. In 2014, the Commercial Bank of Africa partnered with Vodacom in Tanzania to start M-Pawa services, a replica of M-Shwari. Then, the CBA Bank teamed up with MTN in Uganda to develop and customize the Mo Kash services for Uganda and Rwanda in 2017, the bank to bank partnership in Côte d'Ivoire to create the Mo Kash mobile service via a partner bank in Côte d'Ivoire in the year 2018. The bank's accounts have grown in the five countries to be forty million. CBA offers the loan product at an interest rate of 7.5 percent per month with loans ranging from 100 to 50000, and it uses customer data from the MNO to calculate the customer loan limit. The Bank operations are done efficiently by deploying robust temenos banking software, with a lean team of 20 IT personnel and 60 operational staff. Its services are centralized for the five countries in Nairobi. It makes the mobile banking product to be economically efficient. The report covers the CBA Mobile loans while this study is intended to cover all the commercial banks, and it will be focusing on Kenya only and not in east Africa, as in this study.

According to the financial report KCB, the number of mobile loans disbursed by the bank since 2014 has increased exponentially from 0.4 billion to 54.4 billion in 2019. It has enabled the bank to reduce its operational cost in loan processing and turnaround time. The customers can request loans using the mobile app, USSD, or M-Pesa sim tool. These loans are processed, approved using customer M-Pesa data analytics and loan logarithms. It makes customers perceive the bank's new financial innovation as convenient, fast, and secure, attracting more customers. The bank has come up with multiple digital channels to serve their customer needs through mobile banking, agency, merchant POS, branch teller, internet, ATMs.

The bank also collaborated with CBA and M-Pesa to develop a mobile overdraft product called Fuliza in the year 2019, and it has given out loans of 69.4 billion. The product gained its market relevance and significance because of its perceived ease of use, reliability, security, speed, privacy, operational cost, time-saving, and convenience. All these digital transformations are propelled through mobile banking by utilizing mobile phones and smartphones to exploit the internet to download smart banking apps. They have helped achieve the profitability of KShs 25.2 billion in net income through operational cost efficiency and growth in Digital Financial Services (DFS). This incorporates mobile banking as a critical player in the number of registered mobile banking accounts, mobile banking loans disbursed, mobile banking deposit made, and other mobile banking-related services, optimizing the cost while maximizing the profits. The commissions' interest income, fees, and additional revenues increased from 76175 million in 2015 to 102,521 million in 2019, according to the 2019 financial report. Analyzed mobile banking credit on commercial banks' operational efficiency in Kenya [5]. The study's objective was to establish the impact of digital loans on commercial banks' operation efficiency in Kenya. The research adopted an experimental research design. The study used both primary and secondary data on mobile phone credit access on the impact of financial institutions' performance. They found out that mobile loans enhanced operational efficiency in commercial banks. Transferable banking credit has improved operational efficiency in loan processing, approval, and debt collection. They noted that the employment of technology in commercial banks is a consumer-driven approach, cost optimization, and revenue maximization. The study used return on asset, non-performing loan proportion, and earnings per share to measure mobile loans' impact on commercial banks' operational efficiency. The research concluded a significant favorable effect between mobile loans and operational effectiveness on commercial banks in Kenya. This study covered five years between 2010-2015, and it used both primary and secondary data, and it used an experimental design, sampled only five banks, but this study will cover nine years between 2010-2018, it will use secondary data, and it will use census survey. It will cover all the commercial banks in Kenya; hence the research will cover the other areas not covered by the study on mobile credit only and operational efficiency. Mobile banking's effect on commercial banks' financial performance in Kenya to determine the impact of mobile banking loans on commercial banks' performance. The study focused on commercial banks' performance. It applied descriptive and mixed research design using primary data collected through a structured questionnaire and secondary data with a sample of 14 banks. The study concluded that mobile banking loans have a fragile positive correlation relationship implying that commercial banks are introducing faster mobile banking loans to their customers. These affect commercial banks' performance gradually as customers adopt them compared to traditional banking. The research in this study will look at all the commercial banks and use secondary data for nine years, which will be enough to overcome the limitations in this study and test if mobile banking loans have been accepted and what impact do they have on the commercial banks' operational efficiency and not performance.

Variable and model

The research study was anchored on the variables. Operational efficiency as the dependent variable and mobile banking loans as the independent variable. Technology is helping commercial banks to automate their processes, and it allows banks to reduce operational cost. At the same time, they are optimizing technology to maximize their revenue generation. The number of mobile loans or credit and advances offered by the commercial banks serves as a revenue source in terms of loan interest, processing fees, commission, and other related charges. Still, it is the cost incurred to access these loan services while using commercial banks' mobile financial banking services to the customer side. As the number of bank loans increases, the banks can make more revenue with the reduced operational cost because mobile loans are processed; approved using data analytics algorithms customers prefer mobile loans because they are issued instantly and require no guarantors. All loan processes are digitized with no paperwork as compared to traditional banking. The commercial banks can operate optimally by looking at the ratio of non-performing loans. This is done by dividing the provision for non-performing loans divided by the total amount of loans and other advances issued to the customers. This ratio will be a good indicator of how commercial banking operates on loans issued through mobile banking, which can operate optimally or increase the cost of loan recovery and provision for non-performing loans. Mobile banking and commercial banks' operational efficiency of commercial banks in Kenya. The efficiency ratio will measure the operating effectiveness of commercial banks. The efficiency ratio is the ratio between operational expenses and revenue (Figure 1).

Figure 1. Conceptual framework of variables.

The study used a descriptive research design. According to research, design is the systematic plan on the set criteria for data gathering and analysis of data collected to serve this research's purpose. It constitutes the structure within which the study is anchored, and it is the road map for data collection and analysis. Descriptive design is best suitable to describe the elements as they exist under this study, on the effects of mobile banking on commercial banks' operational efficiency. The descriptive design will precisely narrate the attributes of the phenomena under investigation. The plan also demonstrated the relationship between the dependent variable and independent variables.

The target population for this study was the entire commercial banks in Kenya, which is 44 banks, according to the central bank of Kenya report. By the year 2018, some banks have experienced some financial challenges, and some are under statutory management like Charterhouse Bank Limited (CBL). The other two under receivership are imperial bank Ltd, and chase bank limited was excluded from the target population. The study targeted 41 commercial banks classified into three tiers.

Target population

The target population for this study will be the 41 commercial banks in Kenya excluding the ones under statutory management (Table 1).

| Tier | Number of banks (Population) |

|---|---|

| Tier I | 6 |

| Tier II | 14 |

| Tier III | 21 |

| Total | 41 |

The study used a census survey, and thus all the 41 commercial banks were targeted. In this case, the researcher covered all commercial banks under the supervisory of Kenya's central bank from 2010 to 2018, excluding those three banks under receivership or statutory management.

The data collected included mobile banking accounts for nine years, mobile banking loans. The mobile banking deposits, the OE (Operational Efficiency Ratio), was the ratio between operating expense divided by revenue, not including interest every financial year.

Diagnostic test

The table below summarizes on how diagnostic test for the panel data will be done (Table 2).

| Test | Test applied | Conclusion |

|---|---|---|

| Random effect model or fixed effect model | Hausman test | If the p-value is less than 0.05, then there is endogeneity and therefore ignore the random-effects model and employ the fixed effects model. |

| Use of random effect model or pool OLS | Lagrange Multiplier (LM) breusch-pagan |

If the p-value>0.05 apply pooled OLS model. |

| Autocorrelation test | Wooldridge drukker test | If the p-value>0.05, no serial correlation. |

| Heteroskedasticity | Breusch pagan test | If the p-value is less than 0.05 then there is heteroscedasticity. |

| Normality test | PP and QQ plots | Check if the residues are normal on the plot graphs. |

The descriptive statistics results indicate that the commercial banks' maximum operational efficiency ratio since the year 2010 up to the year 2018 is on an overall maximum of 348.16% and a minimum of 17.08% with an overall mean of 65.29%. The operational efficiency of the commercial bank has increased over this period of nine years. This study's standard deviation on the operational efficiency of commercial banks overall is 38.10% with between being 31% and within being 22%. It is prudent to note that the operational efficiency ratio measures how commercial banks utilize technological innovations resources, like mobile banking, to optimize their income while minimizing their operational cost by digitizing their loan application processes, approval and collection. Account opening allows access to; bank deposits, account balance checking, bill payment, and other mobile banking associated processes, which make the commercial banks, reduce their operational cost and generate more revenue in terms of fees, commissions, and interest on loans. This allows leveraging the mobile banking technology and serving customers in their comfort zone. The effect of mobile loans, which is indicated by the non-performing ratio, has a mean of 10.56 and a standard deviation of 9.5 with the minimum of -0.64 and maximum of 47.58 ratios for the provision of the bad debts, which in turn reduces the revenue generated, hence affecting the commercial banks' revenue. It also increases terrible debt provision, which increases the operational cost. Some of the loans provided in terms of bad debt provision are the mobile loans given without any collateral security.

Diagnostic test

Multicollinearity test Pearson correlation among variables: The research study carried out the variables correlation matrix analysis and the analyzed data results from Stata. From the findings, we can conclude that there is no significant correlation among the variables under the study, because the highest R-value is 0.2357 has a medium relationship, which is less than 0.5 hence weak correlation relationship among the variables.

Testing for autocorrelation: The study carried out the panel data autocorrelation test using the Wooldridge test, and the result is shown below. The p-value 0.2193>0.05 means, there is no serial correlation for the panel data.

Normality check: Checking if the residuals are normally distributed, so we use PP-plots and/or QQ-plots (Figure 2).

Figure 1. Normality check for residuals.

Model selection

The research study selected panel data analysis, and there was a need for the selection of the best model which can be employed in this study; the Hausman test needs to be done. It is carried out to determine whether we can use the random effect model or the fixed effect model. Carry out the simple regression model among the variables, the pool model, and then carry out the fixed effect model regression by running the regression model. Then, use the fixed-effect model. Run estimate store fixed command to store the fixed effect model.

From the Hausman test carried out on. The conclusion we can make from the Hausman test is that we can choose the fixed effect model because of the value is p=0.0022<0.05, means, we accept the fixed effect model and reject the random effect model (Table 2).

Data processing and analysis

The study adopted panel data to analyze the findings using STATA software. Data was modeled into a regression equation that defined the relationship between the independent variables and commercial banks' operational efficiency. STATA software was employed to analyze and give descriptive statistics outputs essential for the study that used descriptive research design.

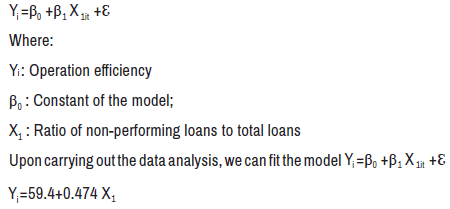

The study model was specified as

Where 59.41 is the operational efficiency for commercial banks when all other variables are not in 0.474 is the increase in operational efficiency in response to a unity increase in bank loan.

Hypothesis test

The mobile loans and commercial banks operational efficiency in Kenya: The p-value for mobile bank loans is 0.017<0.05; hence the null hypothesis: There is no significant relationship between mobile banking loans and the operational efficiency of commercial banks in Kenya is rejected. This means that the relationship between mobile bank loans and commercial banks' operational efficiency in Kenya is statistically significant.

The study found out that there is a positive relationship between the mobile banking loans which is 0.474, and the operational efficiency of commercial banks in Kenya. The study found out that there is a positive relationship between operational efficiency and bank loans. This is due to the introduction of mobile loans introduced by commercial banks to enable the customers to request bank loan, access their loan, and make payments using their mobile phones. The study found out this was the only variable the was significant with the p-value of 0.017, which is less than 0.05; hence, rejected the null hypothesis of the study, which stated that there is no significant relationship between mobile banking loans and operational efficiency of commercial banks in Kenya. The introduction of mobile banks affects commercial banks' operational efficiency. This can be observed in the way the loan request, processing, and approval are made. It takes a few minutes to access your loan due to mobile banking technology, which uses customer data and applies data analytics to approve these loans. The study has found out that bank loans have a significant effect on commercial banks' operational efficiency. The study agrees with, who carried out a study on mobile credit's effect on commercial banks' operational efficiency in Kenya [5]. They utilized the non-performing loan, which we also used in the study. The study concluded that mobile loans or credit have a significant effect on commercial banks' operational efficiency in Kenya in terms of processing approval and repayment and default management.

The research study found out that statistically, the R square was small, which means that the study can expound a small percentage of the study variables; mobile loans in commercial banks operational efficiency and that these research variables cannot explain a larger percentage of the variations.

The research study sought to determine the effect of mobile loans on the commercial bank's operational efficiency in Kenya. The analysis result indicated a positive relationship between mobile banking and commercial banks' operational efficiency. The p-value for the study is less than 0.05. We rejected the null hypothesis, which stated that there is no significant relationship between mobile loans and commercial banks' operational efficiency in Kenya. We accepted the alternative hypothesis, which stated a significant relationship between mobile bank loans and operational efficiency in Kenya. The study established that customers take mobile loans using their mobile phones. This will lead to an increase in the loan amounts issued by commercial banks. This will increase the revenue generated while reducing operational costs like manual loan processing, paperwork, and human resource cost. This has been replaced by mobile banking technology. There is an increase in non-performing loans, which reduces the commercial banks’ profits and increases debt management due to some people taking loans and defaulting.

The study can conclude that bank loans have a positive relationship with commercial banks' operational efficiency in Kenya. This factor was found to have a significant effect on the operational efficiency of commercial banks in Kenya. The mobile loan enables commercial banks to maximize their revenue through interest charges, fees, and commissions. Even though it is increasing the number of loans and other revenues, it is also increasing the nonperforming loans, which reduces the commercial banks’ profits. The financial innovation on mobile banking has improved loan application, access, processing, and approval. It has improved mobile deposit mobilization, which affects the operational efficiency of commercial banks in Kenya.

From our study, we can recommend that commercial banks invest more on mobile loans since it had a positive relationship with commercial banks' operational efficiency in Kenya. Following the current trends in the adoption of financial innovation, commercial banks must invest in digital retail banking to improve their operational efficiency. This can be done by channeling more investment resources to a financial channel to optimize the revenue generated while minimizing cost. A good example is a Commercial bank of Africa M-Shwari product, KCB-M-Pesa, Equitel for equity bank, and Fuliza product, a collaboration of Safaricom KCB and Commercial Bank of Africa. Commercial banks can increase their liquidity through mobile saving and generate more revenue on fees commission’s charges on other financial services like pay bills, account balance, funds transfer, and mobile loans.